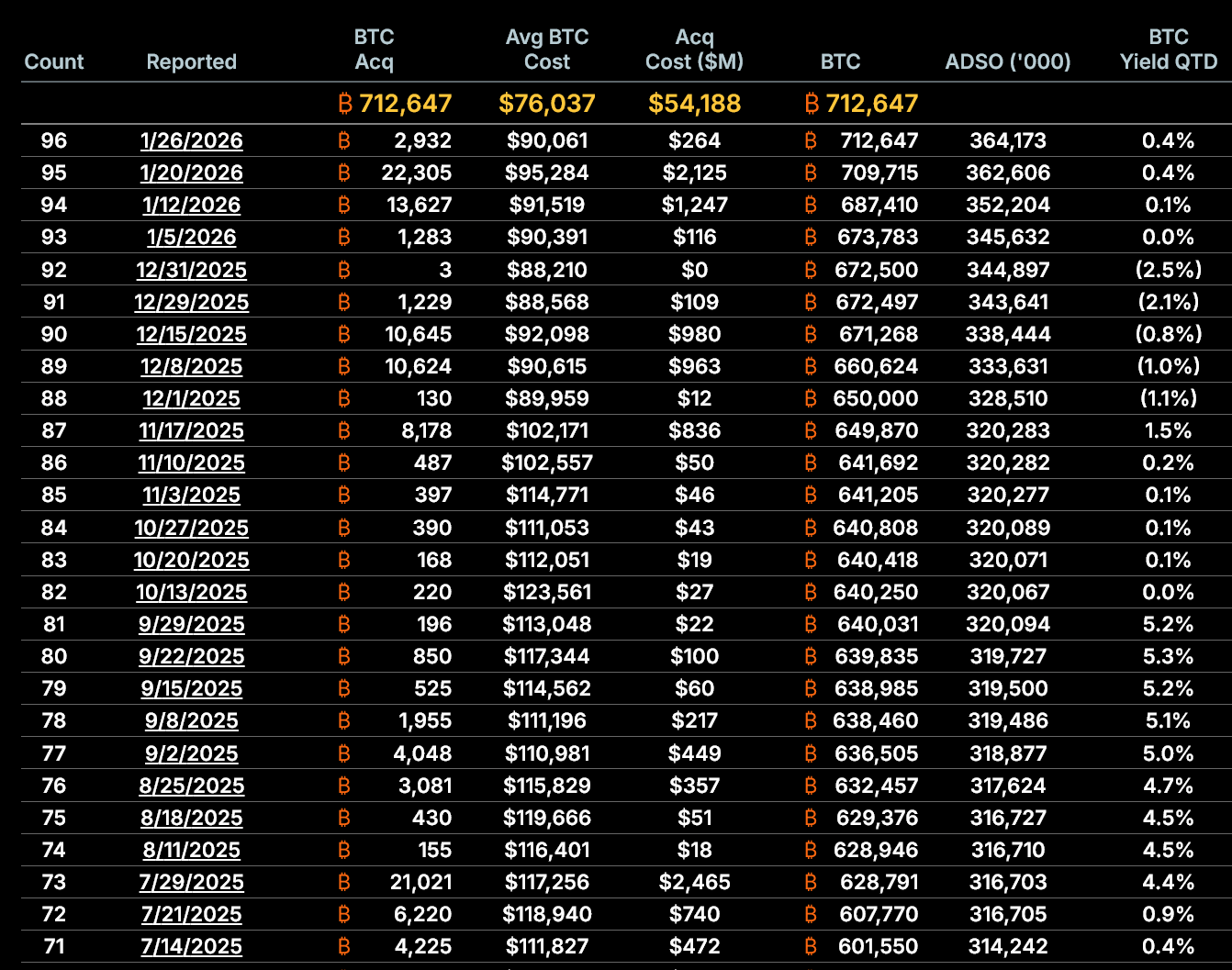

MicroStrategy disclosed its latest Bitcoin purchase on January 26. In its 4th purchase of the month, the company acquired $264.1 million in Bitcoin at an average price of $90,061 per BTC.

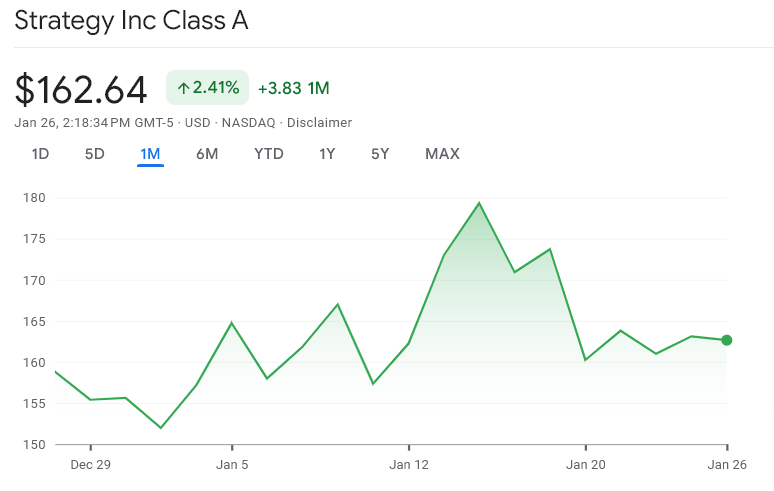

The acquisition brings the company’s average cost of Bitcoin purchase to $76,037. The purchase came as Bitcoin traded in a volatile January range, slipping from early-month highs above $95,000 to the high-$80,000 range.

Latest Buy Details and Funding Structure

While the headline buy reinforces MicroStrategy’s long-term Bitcoin conviction, underlying data suggests the company’s funding model is facing mounting structural pressure.

MicroStrategy funded the January 20–25 purchase window primarily through equity issuance.

The company sold 1,569,770 shares of common stock, generating $257.0 million in net proceeds, alongside 70,201 shares of STRC preferred stock, which raised an additional $7.0 million.

Total proceeds of $264.0 million closely match the reported Bitcoin purchase cost.

In simple terms, Strategy paid for the purchase by selling new shares, not by using business profits or cash on hand.

Most of the money came from issuing common stock, with a smaller portion raised through preferred shares.

Together, these sales fully covered the cost of the Bitcoin purchase. So, the company continues to rely on capital markets to fund its accumulation strategy.

mNAV Has Slipped Into Discount Territory

MicroStrategy’s most critical structural metric is its multiple to net asset value (mNAV), which measures how its equity trades relative to the value of its Bitcoin holdings per share.

As of January 26, MicroStrategy’s diluted mNAV stands at approximately 0.94x, meaning the stock trades at a 6% discount to the Bitcoin backing each share.

This matters because MicroStrategy’s strategy depends on issuing shares above net asset value. When shares trade at a discount, new issuance risks destroying, rather than creating, shareholder value.

Accretive Issuance Is Approaching Zero

Historically, MicroStrategy justified equity issuance by increasing Bitcoin per diluted share. That accretion is now fading.

Based on company-reported data:

- On January 5, MicroStrategy held 673,783 BTC with 345.6 million diluted shares, or 0.001949 BTC per share.

- By January 26, holdings rose to 712,647 BTC, but diluted shares climbed to 364.2 million, resulting in 0.001957 BTC per share.

That represents only a 0.38% increase over the month.

More importantly, between January 20 and January 26, the amount of Bitcoin backing each share barely changed.

This shows that recent share issuance is no longer increasing Bitcoin exposure for shareholders in a meaningful way

Bitcoin Per Diluted Share Over Time

Rising Dilution Is No Longer Offset by BTC Growth

Dilution is accelerating. From January 5 to January 26:

- Diluted share count rose by 5.36%.

- Bitcoin holdings increased by 5.77%.

While holdings still marginally outpaced dilution over the full month, the gap narrowed sharply in the most recent week. This erosion aligns with the fall in mNAV and suggests the model is losing efficiency.

If the stock remains below net asset value, further equity issuance would mathematically reduce Bitcoin exposure per share.

Capital Market Dependence Is Increasing, Not Falling

Strategy’s Bitcoin approach remains entirely dependent on access to capital markets.

Over the past 19 months, the company has raised an estimated $18.56 billion through common equity issuance, issuing approximately 226.6 million shares. The latest purchase continues that trend, adding further dilution at a time when market conditions have weakened.

The company also increasingly relies on preferred stock, which introduces fixed claims senior to common shareholders.

While preferred issuance can sustain Bitcoin buying during equity weakness, it raises long-term obligations and increases balance sheet complexity.

What This Means for Investors

MicroStrategy’s latest Bitcoin purchase is not problematic because of its size or timing. The concern lies in structure, not conviction.

With mNAV now below 1.0x, Bitcoin-per-share accretion nearing zero, dilution accelerating, and reliance on capital markets deepening, the company’s core strategy faces tighter constraints than at any point in recent years.

Unless equity premiums return, continued Bitcoin accumulation risks shifting from accretive to dilutive.

That transition would fundamentally change the risk profile for shareholders, even if Bitcoin prices recover.

For now, the data shows that MicroStrategy can still buy Bitcoin. The open question is whether it can keep doing so without eroding shareholder value.

The post Why MicroStrategy’s Latest Bitcoin Purchase Is Deeply Concerning appeared first on BeInCrypto.