Strategy (formerly MicroStrategy) founder Michael Saylor has piled up cash for over two years of dividend payments and claims that the company can survive a bitcoin (BTC) crash all the way to $8,000.

Although the company itself might survive that crash, common shareholders will actually lose every last theoretical claim to the company’s treasury below a BTC price of $20,094 — far higher than Strategy’s $8,000 corporate survival threshold.

Claims on Strategy’s BTC are, in actual fact, entirely theoretical.

Despite the company’s proud publication of metrics like BTC per share (BPS) or multiple-to-Net Asset Value (mNAV), its lawyers carefully disclaim that neither common nor preferred shareholders have any redemption right to Strategy’s treasury.

No publicly-traded Strategy stock confers any ownership interest in the BTC the company holds.

Nonetheless, MSTR shareholders often talk about BPS or mNAV as shorthand, colloquial valuation metrics for their shares.

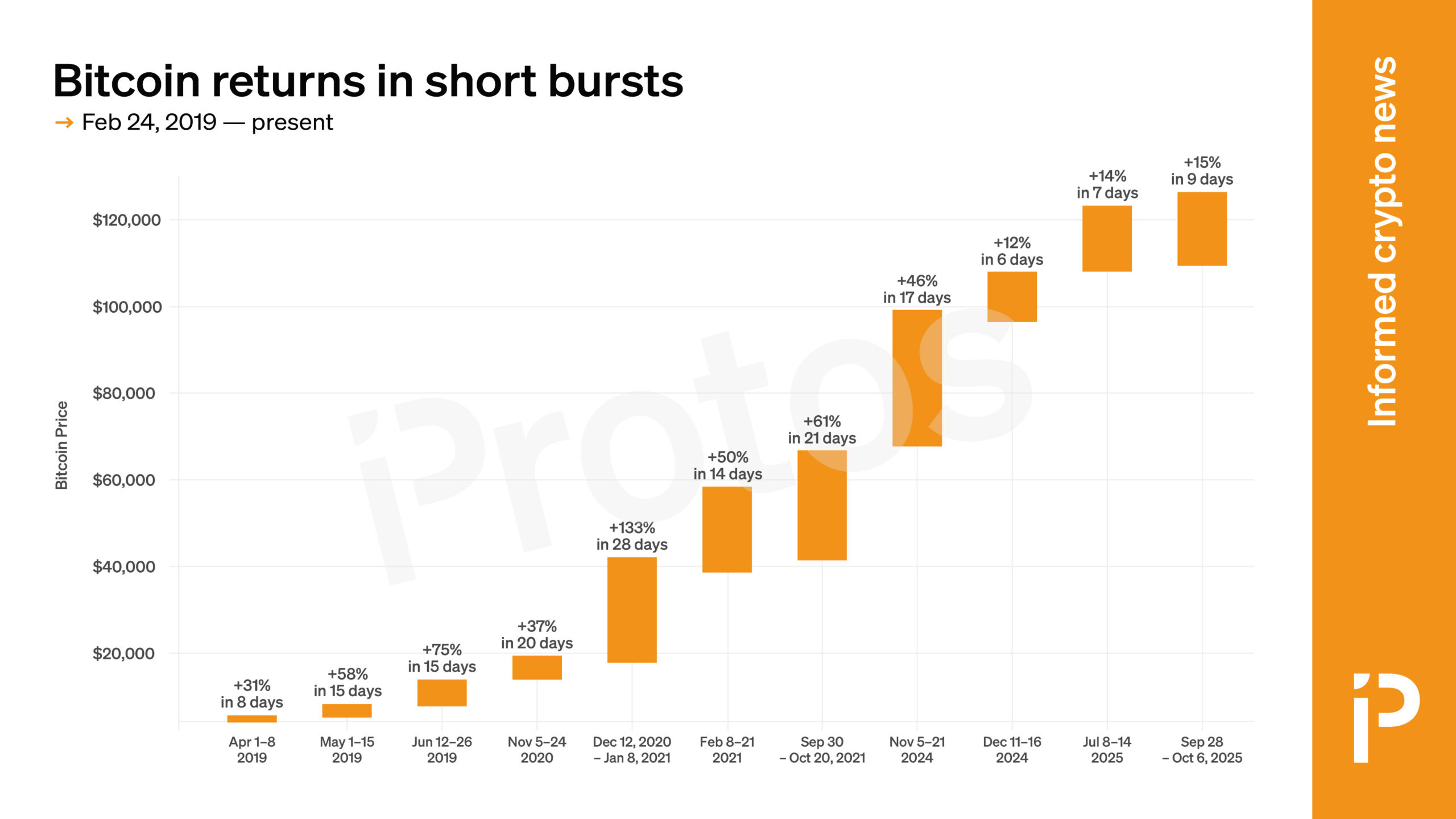

To that end, with BTC down over 40% in just six months and crashing below $63,000 last night, it’s worth recalculating the value of MSTR, the common stock of the world’s largest BTC treasury company.

In our brand new sit-down, I handed @saylor every anti-Bitcoin argument the internet has and he responded to ALL of them.

— Natalie Brunell

I dare any Bitcoin critic to watch this interview and not reconsider at least one of their arguments.

TIMESTAMPS:

00:00 Michael Saylor address Bitcoin bear… pic.twitter.com/lmMnZ2p7WX(@natbrunell) February 23, 2026

$16.672 billion in senior claims above MSTR

Today, there are $16.672 billion in senior claims above MSTR on Strategy’s capital stack: $8.214 billion in debt and $8.459 billion in preferred shares.

Although preferreds don’t mature, they’re senior to commons in the event of bankruptcy. The company must also make $896 million in annual interest and dividend payments, not to mention salaries, compliance obligations, legal expenses, and other costs to service real estate, equipment, and payables.

As assets for all of its series of stock outstanding, Strategy owns a small software business, 717,722 BTC, and $2.25 billion in cash, worth a combined $47.65 billion at a BTC price of $63,270.

This is excluding the small software business that was worth less than $1.8 billion for the three years prior to Strategy pivoting into becoming a BTC acquisition company.

If BTC were to fall below $20,094, bondholders and preferred shareholders would consume the entire value of the company’s BTC and USD treasuries, leaving no claim for MSTR beyond residual, pure call option-like premium on the hope that BTC might rally again.

Read more: 100% of Strategy’s convertible debt is now out-of-the-money

MSTR can wave goodbye to Strategy’s treasury below $20,094

At $20,094 per BTC, the value of Strategy’s 717,722 BTC and $2.25 billion would equal its convertible and preferred claims of $16.672 billion, leaving nothing for MSTR.

Perhaps the software business might cushion a few hundred dollars more per BTC, although it’s been declining in both top and bottom line performance for years.

In any case, the calculation as to what BTC level consumes the entire treasury above MSTR on Strategy’s capital stack is a revealing exercise in basic accounting. Although Strategy prefers its own, self-serving calculators and dashboards, alternative tools exist to recalculate those figures using more conservative assumptions.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The post $63K to $20K: The price range that decides MSTR’s fate appeared first on Protos.