Crypto market liquidity is increasingly hyper-concentrating within a handful of massive trading venues, creating a market structure that global central bank researchers warn is evolving into a heavily leveraged “shadow crypto financial system.”

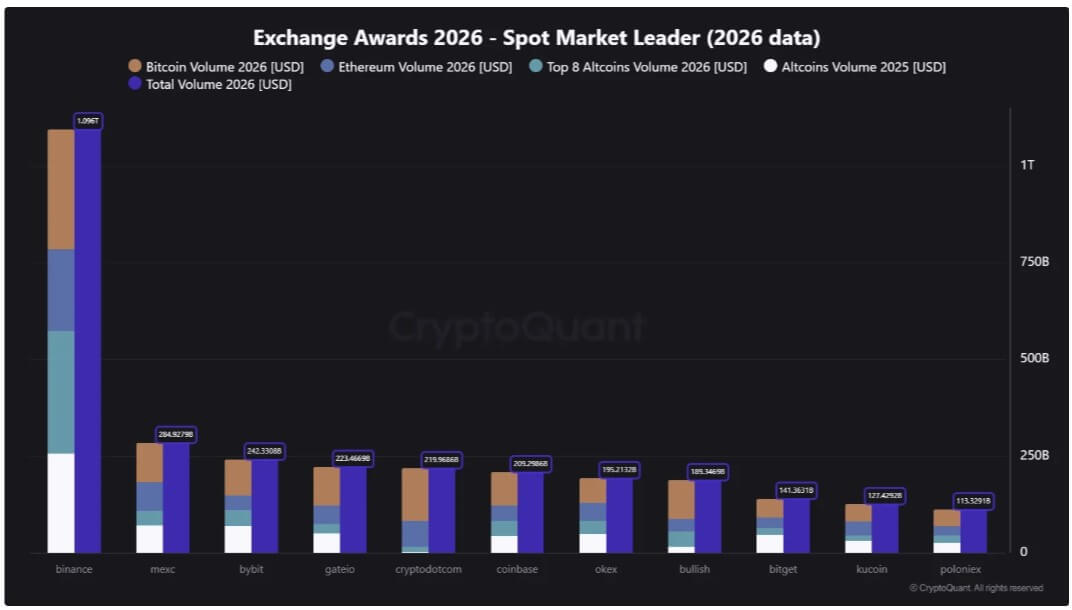

Data from CryptoQuant shows that Binance, the world’s largest crypto exchange, cleared over $1 trillion in trading volume during the first 112 days of 2026.

This is significantly higher than the total of rival platforms like MEXC, which stood at about $284.9 billion; Bybit at $242.3 billion; Crypto.com at $219.9 billion; Coinbase at $209.3 billion; and OKX at $195.2 billion.

The gap gives a market anchor to a new Financial Stability Institute paper published by the Bank for International Settlements, which said large crypto platforms have expanded beyond trading and custody into yield products, lending, derivatives, staking, and token-related services.

The paper described many of these trading platforms as “multifunction cryptoasset intermediaries” (MCIs) because they now combine roles that are usually split among banks, brokers, exchanges, and custodians in traditional finance.

Due to this, BIS flagged concerns that the crypto trading venues attracting the deepest liquidity are also becoming the places where users store assets, post collateral, take leverage, and seek yield.

That has turned the current exchange concentration into a wider question for regulators: whether platforms built for crypto trading have become financial intermediaries before the rules around customer assets, leverage, and liquidity risk have caught up.

Liquidity is concentrated where risk is rising

Crypto’s trading base has not spread evenly across hundreds of platforms despite years of exchange failures, enforcement actions, and market drawdowns.

The BIS paper said there were about 200 to 250 active centralized spot exchanges as of 2025, but trading remained dominated by a small group of large platforms.

BIS pointed out that Binance accounted for about 39% of global centralized exchange spot volume, while the top 10 exchanges handled about 90% of global trading activity.

The BIS paper said the largest MCIs often operate through subsidiaries or licensed entities across more than 100 jurisdictions. It also cited estimates that the top five MCIs collectively serve about 200 million to 230 million unique users, with 20 million to 34 million using staking or earn products.

That means the biggest crypto exchanges are no longer just places where buyers meet sellers. They are becoming balance-sheet hubs for a market that still lacks many of the legal protections built into traditional finance.

That structure gives the largest venues power beyond ordinary market share as their order books influence pricing and their derivatives products shape leverage.

At the same time, their custody systems hold the assets customers use to move across spot, margin, staking, and yield products.

Binance’s $1.09 trillion in early-year volume shows the force of that network effect. Traders continue to cluster where liquidity is deepest and execution is most reliable.

In normal conditions, that concentration can reduce friction. During stress, it can make a handful of venues central to the way losses move through the system.

Exchanges are becoming financial supermarkets

The business model that has made large exchanges commercially powerful is the same model now drawing scrutiny.

A major crypto platform can offer spot trading, perpetual futures, custody, staking, lending, secured borrowing, wallet services, and yield products under one roof. Some also operate affiliated token ecosystems or infrastructure tied to their broader platforms.

In traditional finance, those services are usually split among institutions with different capital, liquidity, disclosure, and conduct rules. Banks, brokerages, exchanges, clearinghouses, and custodians each sit inside specific regulatory lanes.

Crypto has moved toward a more integrated model. A user can deposit assets, trade spot tokens, borrow against collateral, open leveraged derivatives positions, and allocate idle balances to yield products without leaving the platform.

That model keeps capital inside the venue. However, it also makes it harder for users and regulators to separate trading risk from credit, custody, and liquidity risks.

The BIS paper said MCIs that accept customer assets through investment programs and use them for lending, market-making, or other activities take on risks similar to those faced by financial intermediaries. Those include credit risk, maturity risk, and liquidity risk.

The difference is that many crypto platforms do not face the same prudential requirements as banks or regulated broker-dealers. They may not be subject to comparable capital buffers, liquidity rules, deposit protection, stress tests, or resolution frameworks.

Yield turns balances into credit exposure

The clearest example is the growth of earn-and-yield products.

These products are often marketed as a way for users to earn passive returns on idle crypto assets.

However, the economic reality can be much less straightforward. Depending on the terms, customers may give the platform control over their assets, allowing those funds to be used for staking, lending, market-making, margin financing, or other activities.

The BIS paper said some arrangements can leave customers with an unsecured claim on the intermediary rather than a protected right to specific assets. In practice, the user may think of the product as a savings account, while the legal exposure resembles a loan to the platform.

That distinction becomes critical in a crisis.

A bank depositor is usually protected by a framework built around capital requirements, liquidity management, deposit insurance, and access to central bank liquidity in extreme cases.

A crypto exchange customer using a yield product may have none of those protections. If the platform cannot meet withdrawals or suffers trading losses, the customer may become an unsecured creditor.

The BIS cited Celsius Network and FTX's bankruptcy as examples of how those weaknesses can surface.

Celsius offered yield products that depended on lending, leverage, and liquidity transformation. When market conditions turned, and customers sought withdrawals, the platform failed.

On the other hand, FTX exposed a different version of the same structural problem, with customer assets, affiliated trading activity, and group-level risk becoming entangled.

Those examples remain important because the largest exchanges today are bigger, more global, and more embedded in crypto market infrastructure than many failed firms were in 2022.

Leverage can transmit stress fast

The BIS warning also extends beyond customer protection into market structure.

Crypto derivatives markets run continuously, use automated liquidation engines, and often rely on collateral whose value can fall sharply within minutes. When leverage is concentrated on the same venues that dominate spot liquidity, price shocks can become liquidation events before human traders have time to respond.

The BIS pointed to the October 2025 flash crash as an example of how fast the system can move. The episode triggered about $19 billion in forced liquidations across crypto derivatives markets and affected more than 1.6 million traders.

The crash showed how tightly connected leverage, collateral, automated risk engines, and venue concentration have become. Notably, some market observers blamed the October 10 incident on Binance's operating practices.

This is because a sharp macro move hit spot prices, resulting in a price decline that weakened collateral. Then, this weaker collateral triggered margin calls, which forced liquidations and deepened the downward price move.

That loop is not unique to crypto, but the emerging market structure can accelerate it.

Large exchanges sit at the center of that process because they host the liquidity, collateral accounts, and derivatives positions through which deleveraging occurs. A brief outage, pricing gap, or liquidity shortfall at a dominant venue can affect more than that venue’s own users. It can influence market prices across the sector.

Regulators face a business model that outgrew the exchange label

Against this backdrop, the policy challenge is that the largest crypto platforms do not fit neatly into existing categories.

A single firm may operate as an exchange, custodian, broker, lender, staking provider, derivatives venue, and wallet infrastructure provider simultaneously. Each activity may fall under a different regulator, or outside clear oversight altogether, depending on the jurisdiction.

As a result, the BIS paper called for prudential requirements for MCIs engaged in financial intermediation. Those could include capital and liquidity buffers, stronger governance standards, stress testing, risk-management rules, and clearer segregation of customer assets.

It also suggested that regulators may need both entity-based and activity-based rules. Entity-based rules would look at the health and structure of the platform as a whole. Activity-based rules would apply to specific services such as lending, custody, staking, derivatives, or yield products.

That approach would mark a shift from treating large crypto firms mainly as trading platforms to more closely aligning them with their surrounding financial conglomerates.

This would now raise questions about how they manage balance-sheet risk, protect customer assets, handle liquidity stress, and how a failure would be contained.

Meanwhile, this issue is becoming more urgent as traditional finance links to crypto deepen through exchange-traded products, institutional custody, stablecoin reserves, and brokerage integrations.

The BIS paper warned that as MCIs become more connected to traditional finance, disruptions at major platforms could have consequences beyond the crypto ecosystem.

The post Trillions of dollars in crypto liquidity is concentrating inside the venues US regulators fear most appeared first on CryptoSlate.